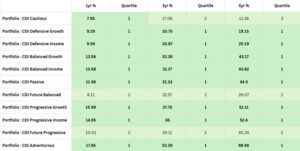

We have previously commented on the growing popularity of passive investment across the industry, and the dangers of relying on a passive only approach when constructing an investment portfolio. This year has, to date, seen major global indices advance, leading to reasonable outcomes for those investing in tracker funds. With global equity indices becoming more concentrated, and the S&P500 and Nasdaq looking fully valued, 2026 could well be the year when active fund management can provide superior performance.

Over the last decade, passive investment funds have grown in popularity, receiving significantly higher inflows than active funds over the last five years. Some in the industry, and many financial “influencers” (whose “advice” we recommend you treat with caution) focus on an evidence-based investment approach, which argues that it is difficult for active managers to beat the market over time, and any strategy should, therefore, be exclusively held in passive investments.

The rise in the popularity of passive strategies is also evident from our own market analysis. Our Investment Committee regularly undertakes a comprehensive review of managed portfolio solutions offered by discretionary fund managers, and our analysis clearly demonstrates that many of our competitor’s products and services carry an increasing bias towards passive investments.

Why passive investments are not the panacea

It is unarguable that passive funds provide a low-cost way of accessing global markets, and they have a place in most diversified strategies; however, we contend that passive funds should be used as part of a broader strategy which includes actively managed funds. Supporters of passive investments fail to take account that a passive investment fund will only track – and never beat – the representative index or market it is trying to replicate. Furthermore, due to tracking errors, most passives lag their target index by a small margin.

Adopting a pure passive approach also means that when the index falls, so does the value of the tracker fund. Unlike a fund with an active manager, who could potentially take avoiding action by reducing allocations, increasing the percentage of cash, or using derivatives, the passive fund will simply follow the representative index.

Over recent years, active fund managers have found it difficult to consistently outperform major global indices, in particular US large cap indices such as the S&P500. Those who champion a passive only approach use such evidence as rationale for their exclusive use of tracker funds. Whilst this has historically been the case, we have noted more actively managed funds investing in the world’s largest market are now producing outperformance over the medium term. This trend may well continue if indices fail to make significant headway during 2026.

A well-documented area in which passive investment has limitations are Fixed Income funds which invest in Government and Corporate Bonds. While passive strategies are often primarily associated with Equities, the universe of passive bond funds has expanded significantly over recent years, encompassing UK and Global benchmarks and providing exposure to portfolios comprising hundreds to thousands of individual bond positions.

Whilst these funds provide broad market exposure, our experience shows that active Strategic Bond managers, who can adjust duration exposure, and portfolio credit quality, can respond to macroeconomic conditions, monetary policy shifts, and evolving credit fundamentals, to adjust their portfolios to take best advantage of the prevailing and expected conditions.

Why 2026 may be tougher for passives

Whilst global market indices have advanced over 2025 to date, the headline index performance masks a significant variance in performance across different sectors. For example, at the time of writing, the largest seven components of the S&P500 index – Nvidia, Apple, Microsoft, Amazon, Alphabet, Broadcom, and Meta – account for 35% of the index by weight. Whilst robust performance from Tech stocks over the second half of 2025 has helped propel index performance, the valuations of leading names have become stretched in places, and any weakness in the sector will have a disproportionate impact on the performance of the index. Amongst the remainder of the S&P500, there are undoubtedly pockets of value, which can be exploited by an active manager, who can allocate a greater proportion of the portfolio to undervalued positions. By doing so, they may also be able to limit the risk to the downside if market sentiment turns.

Our approach

We always aim to seek out good value for our clients, and our independent status allows us to take an unbiased approach as to the precise blend of funds we select. The FAS Investment Committee undertake considerable research on a sector and region basis when we conduct the regular review of funds that we recommend to clients, which encompasses both active and passive options. As a result, this allows us to select passive funds, where this is appropriate, but blend in active funds where we see outperformance.

Our preference when selecting active funds is to choose managers who adopt a conviction-based approach and have a clear vision as to how their fund is to be positioned. This can often mean investing in a concentrated portfolio, when compared to the representative region or universe of stocks available. We regularly come across actively managed funds that align their portfolio closely to the benchmark index. In most instances, such funds fail to impress, as they levy higher charges for active management, without providing the prospects for outperformance.

Summary

We believe passive investment funds have a place in any sensible portfolio, as they provide a low-cost way of accessing broad market exposure; however, we do not subscribe to the mantra of many in the industry who believe it is the right approach in all circumstances. We continue to recommend clients also gain exposure to good performing actively managed funds which can provide significant outperformance and drive overall portfolio returns.

Whilst passive funds provide a low-cost option, we have secured discounts on a range of good-performing actively managed funds over recent years, where charges are only slightly higher than the passive alternative. We will, of course, continue to negotiate lower fund charges with leading fund houses where possible.

If your investment manager is using a passive only approach, we feel it may be a good time to consider whether this remains appropriate. Speak to one of our experienced advisers to discuss your portfolio asset allocation.