The start of a new tax year heralds further changes to the UK tax landscape, affecting dividends, Inheritance Tax, and tax relief on certain investments. Investors, business owners, and landlords need to be aware of the changes, which naturally bring the tax efficiency of investments into sharp focus.

The changes in detail

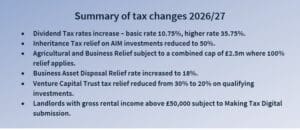

Perhaps the most immediate change investors will notice is that Dividends are now subject to higher rates of tax in the hands of basic rate and higher rate taxpayers. Both rates have increased by two percentage points, with basic rate taxpayers now paying 10.75% on dividend income and a rate of 35.75% applying for higher rate taxpayers. For those who pay income tax at additional rate, the top rate of 39.35% remains unchanged.

With the Dividend Allowance remaining static at just £500, even modest portfolios held outside of a tax-efficient wrapper, such as an Individual Savings Account (ISA), are likely to incur a higher tax charge.

It is not only investors who need to consider the hike in dividend tax rates. Company Directors may well need to reconsider the most efficient way to extract profits from their business.

Following changes announced at the end of 2025, Agricultural Relief and Business Relief is now subject to a combined cap of £2.5 million, up to which 100% Inheritance Tax (IHT) relief can be claimed. Qualifying assets with values above the cap will only benefit from 50% relief (in other words an IHT rate of 20%) which stands in marked contrast to the position before 6th April when an unlimited value of assets could qualify for either Agricultural or Business relief. The combined £2.5m allowance for qualifying assets is transferable between spouses and civil partners, which is a welcome change from the original draft legislation announced in 2024, and provides the opportunity to consider the ownership of assets.

Shares quoted on the Alternative Investment Market (AIM) will now only benefit from 50% relief making the effective IHT rate 20% on these assets. As a result of these changes, those holding AIM investments may wish to rethink whether accepting a lower rate of IHT relief is significant justification for continuing to hold AIM investments or consider alternative investments that benefit from relief.

The sale of business assets, which qualify for Business Asset Disposal Relief (BADR) will now attract a rate of 18% on gains, an increase of 4% on the rate which applied in 2025/26 and significantly above the 10% level which applied before 2025. The lifetime limit for capital gains which qualify for BADR remains at £1m in the new tax year.

Income tax relief on Venture Capital Trust (VCT) investments has been cut from 30% to 20%, which represents a blow to smaller businesses, who rely on VCT funding, and skews the ratio of risk and reward when investing in fledgling unquoted UK businesses. At the same time as reducing the tax relief, other VCT rules have been relaxed, which allow larger and more established companies to apply for VCT funding. Over time, these changes may well improve the quality of VCT portfolios and reduce risk. In the intervening period, we wait to see the impact of the reduction in income tax relief on the ability of VCT managers to successfully raise funds.

From 6th April 2026, landlords with gross annual rental income exceeding £50,000 are required to maintain digital records and submit quarterly updates to HMRC, under Making Tax Digital, in addition to completing their annual tax return. The scope of the regime will broaden significantly in the coming years. Landlords with gross rental income above £30,000 will fall within its requirements from April 2027, with the threshold reducing further to £20,000 from April 2028.

Practical steps to take

The changes introduced from 6th April will see higher rates of tax applying to dividends and allowances reduced. There are, however, practical steps you can take to be more tax efficient.

The simplest step is to make sure that you use all available tax allowances. The annual ISA allowance remains at £20,000 for all investors in the 2026/27 tax year and dividend income earned from investments held within an ISA is tax-exempt. Whilst the Dividend Allowance may well be modest at just £500, married couples can arrange their investments held outside of a tax wrapper carefully to ensure that both allowances are used.

Looking further ahead, the income tax rate on savings income is due to increase from April 2027, and pensions will enter the scope of IHT from the same date. Planning now, rather than reacting later, can help build greater tax-efficiency and strengthen your financial position.

The benefit of personalised advice

The new tax regime has introduced further changes that investors and business owners need to consider. Whilst we have set out practical steps you can take, personalised and individual financial advice can deliver significant benefits. Our experienced advisers at FAS can consider your personal financial situation and provide independent advice on effective ways both to reduce your tax burden and ensure your investments, pensions and other arrangements are professionally managed and reviewed.

If you would like to discuss how the changes affect you, we would be delighted to start that conversation.