Over the course of a working life, most of us accumulate pension pots scattered across multiple providers. Moving between jobs usually leaves behind a deferred pension arrangement and depending on the length of service with any single employer, this may result in several small pots that are difficult to track, monitor, and plan around.

As a result, it may be tempting to combine these pots together into a single arrangement to simplify your retirement planning, which can prove beneficial; however, pension consolidation is certainly not right for everyone, and careful consideration is needed before taking any action.

Benefits of consolidation

Perhaps the most immediate improvement pension consolidation can bring is clarity. By holding a single pension arrangement, rather than pots with different providers, you can readily understand the combined value of the personal pension arrangements, making it far easier to track performance. Holding a single pension arrangement can also bring administrative benefits, too.

The low-cost platform pensions available today bear little resemblance to older style pension arrangements. Many contracts arranged in the past carry high annual management charges when compared to their modern equivalents. We often come across legacy pension arrangements where annual management charges of 1% per annum or more are levied, on top of monthly plan fees. When compared to the cost of modern style pension arrangements, the additional charges levied can eat into investment returns, which compound over many years.

Pension legislation has seen many changes over the last decade, and those reaching retirement now have a greater choice when deciding how to draw pension benefits. Older pension arrangements which pre-date the legislative changes may not provide the full range of options available to newer pension plans, and limit access to features that could increase income and aid tax-efficiency in retirement.

Another stark contrast between older pensions and modern contracts is the range of investment options. When assessing an existing client’s pensions, we frequently review legacy plans that offer a very restricted range of investment funds, which seldom offer reasonable performance. Modern pension contracts typically offer access to a much wider choice of funds, from passive to actively managed, and open architecture platforms provide access to funds from across the whole of the market. From the additional choice available, it is far easier to construct a portfolio that aims to outperform over the longer term.

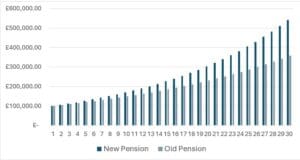

To demonstrate the impact of charges and performance over the longer term, take the example of Richard. He is aged 35, and is looking to review his deferred pension, seeking improved performance and cost efficiency, without altering the level of risk. Richard transfers the deferred pension, valued at £100,000, to a low-cost platform pension and no further contributions are made to the pension post transfer. The transferred plan is invested in a portfolio of good performing funds, and produces a net annual return of 6% per annum (net of charges). The older style arrangement from which he transferred, underperforms the new arrangement by 1% per annum and also carries an additional cost of 0.5% per annum when compared to the charges on the new contract. On reaching 65, Richard reviews the comparative performance of the two pensions and is surprised to see the difference in value between the older, more expensive, pension and his new style arrangement is over £183,000. Put another way, this could provide Richard with an additional £9,000 per annum in retirement via Flexi-Access Drawdown or an Annuity.

The pitfalls

Pension consolidation may provide tangible benefits; however, depending on the arrangements held, disturbing an existing pension can cause financial harm. In particular, some pension contracts established many years ago provided guaranteed benefits, which may be lost on transfer.

Amongst these valuable benefits can include Guaranteed Annuity Rates, which provide the right to convert the pension pot into an annuity that may offer improved rates over those available on the open market, or Protected Tax-Free Cash, where the individual can take more than the standard 25% of the value of the pension as Tax-Free Cash.

The timing of any consolidation exercise also carries risk. Moving pensions between different providers and schemes leads to a period when the pension funds are not invested. This “time out of the market” could work in either direction depending on the performance of underlying market conditions, and therefore it is important to ensure that the period when not invested is kept to a minimum.

When to consolidate

Many people leave pension consolidation until the run-up to retirement, when the focus on providing an income in later life sharpens. Streamlining existing pensions as you near retirement can be highly beneficial, as building a cohesive retirement strategy across multiple plans often adds complexity. That said, given the potential benefits of lower costs and improved prospects for performance, consolidating deferred pensions after a change of job may also be a sensible course of action; however, if you are still an active member of the pension you look to transfer, this may lead to loss of employer pension contributions. It is, therefore, sensible to leave any consolidation until you have left employment and have ensured that no further contributions are due to be paid into the pension.

The importance of advice

Accumulated pension savings represent contributions made throughout a working life and form the backbone of many retirement plans. It is, therefore, important to seek appropriate advice before considering whether to take action on deferred pensions, to avoid making a potentially costly mistake.

Our experienced advisers can carry out a full audit of your existing pension arrangements and provide an independent and unbiased assessment of the features, fund availability and performance, and retirement options. We can access low-cost platform pension arrangements offering whole of market fund choice, and all retirement income options available under pension freedom legislation. Speak to one of our team to discuss your existing pensions so that you can plan ahead with confidence.