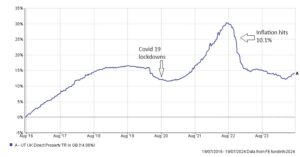

Any long term investment strategy will enter stormy waters from time to time, with the Covid-19 pandemic, Russian invasion of Ukraine and inflationary spiral amongst the factors that have made for a bumpy journey over recent years. Since last November, market conditions have felt considerably calmer, with investors enjoying a period of solid returns. Over recent trading sessions, however, the swell has picked up again, with volatility increasing across global equities markets.

Why have markets outperformed?

The gradual decline in inflation and prospect of easier monetary policy, corporate earnings reports that have largely beaten expectations, and stronger-than-expected economic data have proved the catalyst for the positive market conditions over the first half of this year.

After the hangover from the Covid-19 pandemic, and the Russian invasion of Ukraine, central banks around the World were forced to raise interest rates to head off an inflationary spiral. With inflationary pressures now easing, investors have been eagerly anticipating a change in direction from central banks, as rate cuts are generally perceived as being positive for both companies and consumers alike.

Corporate earnings have also supported the rally seen through the first half of the year. According to Factset, 78% of US quoted companies reported better than expected second quarter earnings, with earnings reports from technology giants reinforcing the positive market sentiment.

The final factor behind the strong performance had been the continued strength of the US economy. Investors have been increasingly hopeful that the Federal Reserve manage to steer a course where inflation moderates, without tipping the US economy into recession.

Reaching the pivot

Recent economic data has, however, stoked fears that central banks could have left their restrictive policies in place for too long. The European Central Bank cut rates by 0.25% in June, and the Bank of England followed suit this month. The Federal Reserve has been keen to ensure that inflation remains in check, and are yet to cut rates, potentially increasing the risk of recession.

Recent US unemployment data has been much weaker than expected, and market consensus now expects that the Federal Reserve may need to take more drastic measures over coming months, to avoid a stall in economic growth.

Where strong earnings reports propelled markets higher over the first half of the year, forward guidance from a handful of tech giants over recent weeks has painted a more mixed picture. The valuations on major tech players are somewhat challenging, and earnings disappointments are likely to weigh heavy on market sentiment.

Away from the tech sector, the first signs of a rotation into more traditional industries have emerged, and renewed focus on value and mid-cap stocks could be a dominant feature over the remainder of 2024.

Seeking value globally

Whilst the performance of US markets sets the tone for global equities, there are always regional variances that provide opportunities. The outlook for the UK remains modestly positive, with an improving picture for growth over coming quarters, and UK equities continue to look inexpensive when compared to global peers. European markets also remain mixed. French stocks remain under pressure due to recent political instability, and general sentiment not helped by tepid Eurozone growth figures.

After a strong start to the year, the Nikkei 225 index of Japanese stocks has seen significant volatility of late, largely due to the strength of the Yen against the Dollar and the impact this may have on exporters. Despite the sharp technical moves in recent trading sessions, Japanese stocks remain attractively valued.

Chinese equities have struggled over the first half of the year; however, there are increasing calls for further stimulus, with additional Government intervention to help boost economic growth becoming more likely. The continued weakness in the beleaguered property sector may however, keep any outperformance in check, at least in the short term.

Geopolitical risks remain

Perhaps the biggest risk to global markets is the outcome of the US election in November. Investors have been weighing up the potential impact of the Trump-Harris showdown with the withdrawal of President Biden closing the gap in the polls. Markets had priced in a convincing Trump victory over recent months; however, the early surge in support for Harris could lead to an increase in market volatility, should momentum for the Harris ticket be sustained as election day draws closer.

The election result is likely to have implications for the conflict between Russia and Ukraine, which remains an ongoing risk to global stability and commodity prices. The US election result will also dictate the future path of US-China relations, where trade tensions continue, and the ongoing threats over Taiwan remain.

Conflict between Israel and Gaza, and wider unrest in the region, have yet to have any material impact on market sentiment. Any wider escalation could, however, push oil prices higher, damaging global economic prospects and fuelling inflation. Any surge in prices could, however, be tempered by weaker global economic growth.

Bond rally to continue?

Weaker economic data over recent weeks has seen bond yields fall (which pushes bond prices higher), and with markets now expecting a series of rate cuts by Western central banks over the next 12 months, the outlook for bonds appears broadly positive. Bond investors will, however, need to consider credit quality, in the event that economic growth slows significantly. The additional yield offered by sub-investment grade bonds does not appear to offer sufficient additional return to compensate for the increased risk of an economic slowdown.

A broadly positive outlook

After enjoying a calm and positive first half of 2024, we have seen greater levels of volatility over recent weeks, and we expect this to continue through the remainder of this year. US equities continue to offer good value over the longer term, although the short-term performance may well be dominated by actions taken by the Federal Reserve. UK and European markets remain cheap when compared to the US, and any renewed focus on value equities could shrink the performance gap between the UK and US.

Diversification remains ever important, and whilst equities markets may see further volatility in the short term, holding an allocation to other asset classes can aid stability. After being adversely affected by the inflationary pressures of recent years, government and corporate bonds look attractively priced, given the monetary easing expected over the next few quarters. Lower interest rates may also prove positive for both commercial property and infrastructure investments, which have underperformed since 2022.

With more volatile conditions seemingly set to return, we feel this would be a sensible time to review the investment strategy within pension or investment accounts that you hold. Speak to one of our experienced advisers to discuss your existing portfolio strategy and consider whether any changes would be appropriate.