Bond yields rarely make headlines outside financial pages, yet few numbers say more about a country’s economic health. UK government bond yields, which have remained stubbornly high since the start of the conflict between the US, Israel and Iran, have risen again over recent weeks, as investors wait for clarity on the spending plans of the new Burnham administration. We look at the challenges facing the new government, and the seventh new Chancellor of the Exchequer in as many years, John Healey.

Factors that affect gilt yields

A gilt is simply an IOU from the UK government. The Treasury borrows money from an investor and promises to pay a fixed rate of interest until the bond matures, at which point it repays the face value. The yield is the effective annual return an investor gets for holding that bond, and it moves in the opposite direction to the price. When gilts are in demand, prices rise and yields fall, and conversely when investors demand a higher return to compensate for perceived risk, prices fall and yields climb.

Government bond yields can rise for several reasons. The prospect of higher inflation acts to suppress investor demand, due to the fixed coupon offered on most government bonds. For example, a gilt offering an interest rate of 5% may look appealing if inflation is running at 1%, but only offers a marginal real return if inflation sits at 4.5%. Gilt supply can also cause yields to rise, as the Treasury may need to lower the price on new issues to attract buyers. Heavy supply of new gilts often signals additional borrowing, which can raise alarm about the ability for the government to service its debts.

Why gilt yields matter

According to the UK Debt Management Office’s Debt Management Report, the UK central government sterling debt stood at £2.9tn at the end of 2025, and gilts make up around 85% of this number. Debt interest will account for almost £110bn in the 2025/26 fiscal year, which is the equivalent of around 3.6% of UK Gross Domestic Product (GDP). Given the size of the debt and interest payable, any marginal increase in gilt yields heaps further pressure on the UK’s public finances, leading to a higher share of tax revenue servicing debt, and tightening the room for manoeuvre on everything from the NHS to defence spending.

The implications of gilt yields go far beyond the government’s own borrowing costs, though that alone is significant. They also set the benchmark for the entire domestic financial system. For ordinary households, elevated gilt yields translate into higher fixed mortgage rates and costlier consumer credit, since lenders price mortgage deals from gilt yields. For savers approaching retirement, gilt yields affect annuity rates, with those purchasing an annuity being one of few beneficiaries of higher gilt yields. Yields on long term gilts can also affect pension fund solvency and impact long-dated corporate finance.

Gilts are also a barometer of confidence in the UK as a place to invest. Britain runs a persistent budget deficit and relies on international investors to buy a large share of the debt it issues each year. Indeed, around one-third of gilts are held by overseas investors. If those investors start to doubt the government’s fiscal discipline and sell their holdings, yields can rise further. It is, therefore, crucial that the new administration can maintain investor confidence.

The new government’s test

Keir Starmer’s resignation and Andy Burnham’s arrival in Downing Street landed at a delicate moment for gilt markets. Burnham takes office as Britain’s seventh prime minister in a decade, a factor in itself, as investors generally prefer stability to persistent change; however, the greatest challenge will be to balance supporting a squeezed British public without spooking the investors who buy Britain’s debt.That balancing act is precisely what gilt markets are pricing. Any hint of looser borrowing plans, without a credible plan to fund them, risks a repeat of the market reaction that forced the hand of the Liz Truss administration in 2022. On the other hand, if the new administration can announce measures that show financial prudence, yields have room to ease, cutting borrowing costs for the government, households, and businesses alike.

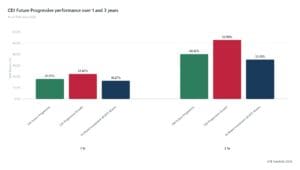

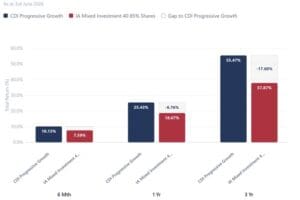

The verdict from investors has, thus far, been lukewarm, with government bond yields rising across the curve since Burnham’s accession. The chart below shows the yield on different gilt maturities (from 2 years to 25 years) with the dark blue line highlighting the yield at the end of July, as compared to the position in July 2025, which is shown in light blue, and one month ago, highlighted in pink.

Actions bond investors should consider

Bond vigilantes will be keenly watching for clues as to the direction of policy decisions by the new administration. Until clarity is reached, expect bond markets to remain cautious. With inflationary expectations already elevated due to the rise in oil and natural gas prices caused by conflict in the Middle East, the outlook for government and corporate bonds remains mixed.

Investors look to fixed interest investments, such as bonds, to add stability to a diversified portfolio, and whilst bonds are often a counterfoil to more volatile equities positions, this isn’t always the case. The sharp fall in bond prices seen during 2022 remains fresh in the memory for many investors, and these conditions could be repeated if the new government fails to convince markets that they have a credible plan.

Through our advisory and discretionary managed portfolios, we have primarily invested in short-dated bonds for more than two years, with the FAS Investment Committee continuing to favour bonds with a duration of less than five years. Choosing short-duration bonds aims to pick up the attractive yield without accepting inflation risk that is present in longer-dated issues. Furthermore, the Committee has looked to avoid bond funds with more than a minor allocation to gilts, favouring high-quality global corporate bonds which offer a yield premium without the political risk.

Speak to one of our experienced independent advisers if you wish to discuss how your portfolio is positioned.

Sources: Bank of England, UK Debt Management Office