In the last edition of Wealth Matters, we explored the changes to tax legislation affecting investors, effective from 6th April 2026, together with practical steps you can take to reduce the burden of tax on your investment returns. Whilst tax-efficiency is an important aspect of any sound financial plan, it should not, however, be the primary driver of investment decisions. Indeed, focusing too much on the potential tax implications of a particular course of action can lead to poor decision making, introduce additional risk and potentially lead to missed opportunities.

Investment decisions

All of us would naturally prefer to receive tax-free investment returns and holding investments within an Individual Savings Account (ISA) provides exemption from income tax on dividends and interest and capital gains tax (CGT) on gains. The annual ISA allowance for stocks and shares investment stands at £20,000, although existing cash ISAs can be transferred to a stocks and shares ISA creating further room for growth in a tax-efficient manner.

Once investments exceed immediately available tax-free wrappers, some investors may choose to limit new investments to the annual ISA allowance and not make further investments, even if funds have been set aside for this purpose.

In most cases, history tells us that this could lead to a worse outcome, even considering the tax deducted on income and CGT on gains on assets held outside of a tax-efficient wrapper, as returns achieved from a diversified portfolio should exceed those available on cash deposit over the medium to longer term.

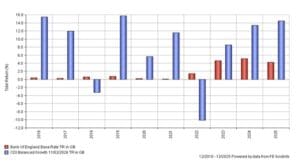

The chart below shows the return achieved each year by the CDI Balanced Growth portfolio, which adopts a medium risk approach (in blue) and the Bank of England Base Rate (shown in red). In eight out of the last ten years, the invested position has comfortably beaten returns on cash, with 2018 and 2022 being the two occasions when cash outperformed. Looking across the last ten years, rather than by calendar year, the cumulative additional gross total return achieved by the CDI Balanced Growth portfolio – as opposed to holding funds as cash – has been 95%. When you place the modest tax implications of investing outside of an ISA against historic outperformance, this serves as a useful reminder that tax considerations should not be a barrier to long-term investment.

Indeed, the tax treatment of investments held outside an ISA is often more forgiving than people expect. The Personal Savings Allowance covers the first £1,000 of savings income for basic rate taxpayers and £500 for higher rate taxpayers, and the Dividend Allowance covers the first £500 of dividend income received. These allowances can catch a proportion of the income generated within a General Investment Account. Beyond these allowances, the rate of tax applying to dividends in the hands of a basic rate taxpayer is 10.75%. Considering this another way, a basic rate taxpayer gets to keep almost 90% of dividend income that exceeds the Dividend Allowance.

As the annual ISA allowance resets each year, a practical solution is to sell investments held within a General Investment Account to fund future year’s ISA allowances. This will achieve greater tax-efficiency over time, whilst keeping funds invested.

CGT – look through a different lens

Another key investment decision where tax should not be the only consideration, is the decision to sell an investment outside of an ISA that will generate a CGT liability. It can be tempting to fall into the trap of choosing not to sell an investment, due to the CGT liability that would be generated; however, it can be helpful to look at the decision through a different lens. An individual who pays basic rate tax would keep 82% of the profits over and above the available CGT exemption and higher rate taxpayers would retain 76% of the profit over and above the exemption. Reinvesting the net sale proceeds into another investment, which then outperforms the investment that was sold, could lead to substantially improved returns, despite the tax bill incurred.

Pensions and Inheritance Tax (IHT)

One of the most frequently discussed areas of financial planning concerns unused pension funds. Under current legislation, pension funds sit outside of your estate for IHT purposes, and in situations when pension income is not needed, it has proved sensible planning to simply leave the pension undisturbed, as it can be passed to surviving spouse or family members without being subject to IHT. This position will change from April 2027, when unused pension funds are brought under the scope of IHT, which will lead to those impacted facing important decisions as to how to deal with existing pension funds. One option is to gift the value of the pension away to family members, and in the case of the Tax-Free Cash, which is usually 25% of the value of the pension up to the Lump Sum Allowance, this decision doesn’t carry any personal tax implications.

Beyond Tax-Free Cash, any pension income whether generated through an annuity or via Flexi-Access Drawdown, is potentially subject to Income Tax in the hands of the pension holder. Even if income is not needed, it may be sensible for a basic rate taxpayer to pay the 20% tax on pension income, and then spend or gift the income, rather than their estate suffer a potential liability to IHT on the unused pension, which is levied at 40%. Paying a smaller tax bill now to avoid a larger one later is a perfectly rational outcome, and a good illustration of why tax should inform decisions, not dictate them.

An impartial view

Whilst tax-efficiency is an important driver of investment returns, there are wider considerations that need to be taken into account. This is where holistic financial planning advice can help in taking an impartial view of your circumstances and provide an alternative perspective, which can help overcome inertia when it comes to taking decisions that create a tax liability. Speak to one of our experienced and independent financial planners to start a conversation.

Source: F E Analytics April 2026