In the weeks ahead, the FAS Investment Committee will produce a series of articles giving further insight into the investment process behind the CDI range of portfolios, focusing on asset allocation, performance and looking at how the range of portfolios meets the differing needs, circumstances, and objectives of our clients. In the first of the series, we go under the bonnet of the CDI Balanced Growth portfolio.

FAS Investment Committee process

Investment markets have experienced significant changes over the 35 years since the inception of FAS; however, in the face of changing market trends, which has driven many to adopt a passive-only approach, we remain firm advocates of the benefits of conviction-based investment. The FAS Investment Committee remain steadfast to these core principles that have guided our investment fund selection for more than three decades, and this investment process forms the foundation of the CDI range of discretionary managed portfolios.

When constructing the CDI portfolios, the Investment Committee use the independent status that FAS enjoys, to consider fund solutions from across the whole of the market. All funds available to UK investors are fed through a quantitative screening process every quarter, which continues to be refined and adjusted. Those funds that pass the filtering process are then rigorously assessed before they can be considered for inclusion within a CDI portfolio. Consistently strong fund performance is, naturally, a key factor; however, the Committee also factor in risk, volatility, concentration risk and costs when creating and refining the CDI portfolios.

Asset allocation

Maintaining adequate diversification is a key consideration when the FAS Investment Committee adjusts the allocations within any of the CDI portfolios; however, the medium risk approach adopted within the CDI Balanced Growth portfolio allows for a very high degree of diversification. The portfolio can invest a maximum of 65% in equities, although the Committee have taken a tactical decision over recent quarters to reduce exposure to US equities, leading to a current equity allocation of just under 55%. Whilst the portfolio will generally allocate 2% to cash, the decisions of the Committee have led to a temporary balance of 6.7% in Cash, which remains productively held in money market funds.

In addition to diversification across asset classes, the CDI Balanced Growth portfolio also allocates funds across all regions of the World. Whilst the Investment Committee are not constrained by geographic limits, the medium risk and balanced approach would ordinarily dictate that a higher proportion of the portfolio will be allocated across developed markets in North America, UK, Europe, and developed Asia.

As is the case in every CDI portfolio, the Committee aim to blend our preferred conviction investment style, through active managers, with passive funds that provide broad market exposure. As a result, the weighted fund charge of the portfolio is 0.35%, which is highly competitive for such a blended investment approach. In addition, the Committee continue to work with leading fund managers to access lower cost share classes where possible, with the aim of reducing the total portfolio cost of ownership.

Portfolio Performance

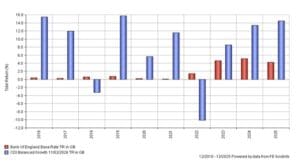

Measuring performance over a five-year period from 1st April 2021 to 1st April 2026, the CDI Balanced Growth portfolio (shown in green on the graph below) achieved a total return of 40.21%, which was more than double the 19.87% returned by the representative benchmark, the IA Mixed Investment Sector 20% to 60% shares (shown in red).

In addition to benchmarking the CDI portfolios against the IA sector benchmarks, we undertake a regular process which reviews our performance against managed portfolio services offered by leading UK portfolio managers. This process aims to ensure our services offer good value for money and performance remains consistently strong against real-world competitors.

Naturally, performance is the key metric on which we, and of course our clients, will focus; however, the level of risk taken to achieve returns is an important consideration. The FAS Investment Committee consider levels of volatility at each quarterly review stage, to ensure that they remain consistent with the levels displayed by the benchmark. Where changes are made to the portfolio each quarter, the impact of the change on the historic maximum drawdown and value at risk is carefully considered.

Practical applications for the CDI Balanced Growth portfolio

As the most popular CDI mandate, CDI Balanced Growth is an appropriate solution for anyone seeking capital growth wishing to take the middle ground between risk and reward. The portfolio’s diversification allows good levels of participation in rising markets, and allocations to investment grade corporate bonds and cash provide balance and aim to reduce drawdown in periods of market instability. This makes the Balanced Growth portfolio an ideal choice for pension funds, particularly in the pre-retirement phase, trusts and applications where capital growth over the medium term is sought.

Whilst not focused on income production, the asset allocation within the CDI Balanced Growth portfolio will lend itself to providing a modest level of income. The natural gross income yield generated by the CDI Balanced Growth portfolio is currently 3.3%, and therefore those who wish to focus on growth, with income as a secondary consideration, are also well catered for.

If you hold an existing investment portfolio – be it within a pension, Individual Savings Account (ISA) or General Investment Account – it is important to regularly review the performance you have achieved compared to alternative managers. Beyond performance, it is also useful to consider the level of risk to which you are exposed and to determine whether you are receiving good value for money. Our independent advisers can undertake an impartial performance review of an existing portfolio and provide an unbiased assessment of performance against the CDI portfolio range. Speak to one of the team to start a conversation.

Source: FE Analytics April 2026