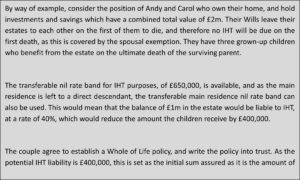

Inheritance Tax (IHT) planning remains a central focus in many financial planning discussions, especially for individuals and families seeking to preserve wealth across generations. A common concern among clients is ensuring that as much of their estate as possible is passed on to loved ones, without being subject to IHT. At the same time, clients often express the wish to retain a degree of flexibility in their planning, enabling them to adapt their arrangements as their circumstances change.

One solution that can offer both tax efficiency and a flexible approach are investments that qualify for Business Relief. Whilst these strategies can be a valuable tool for IHT mitigation, significant changes announced in the October 2024 Budget will impact how Business Relief can be used from April 2026 onwards.

Business Relief basics

Business Relief was first introduced under the Finance Act of 1976. Its purpose was to alleviate the pressure placed on family-owned businesses where, historically, the imposition of IHT on death forced families to sell the business to meet tax liabilities. Over time, the scope of Business Relief was extended to include not only unquoted trading businesses, but also certain companies listed on the Alternative Investment Market (AIM), which is an alternative UK stock market for small and medium-sized innovative companies.

To benefit from Business Relief, shares held must meet specific criteria. The shares must be in an unquoted trading company or a company quoted on AIM and must have been held for at least two years before the investor’s death. In addition, the company in which the shares are held must be actively trading and not primarily involved in investment activities. This means that rental property companies are unlikely to qualify for relief. Finally, excessive cash reserves or non-trading assets held by the investee company may disqualify it from relief, as HMRC may interpret it as an investment rather than a trading business.

Accessing Business Relief through managed solutions

Most individuals are not directly involved in owning or running qualifying businesses—and may have no desire to do so. To bridge this gap, the financial services sector has developed a range of investment solutions that allow investors to access Business Relief investments through managed portfolios, providing the same tax advantages without the need to be operationally involved in a business.

Most managed solutions invest funds in a broad range of different qualifying trades, which focus on asset-backed investments, such as renewable energy facilities – for example wind, solar and hydro power generation – storage and warehousing, commercial property rental and forestry. They generally target modest returns, say between 3% and 5% per annum, which if achieved, would provide an element of inflation proofing.

While these asset-backed businesses can provide more stability than traded equity-based investments, they also carry certain risks. Notably, such investments are unquoted, meaning there is no public market to trade the shares. As a result, they are less liquid and may be more difficult to value or sell quickly. Investors must understand these risks as part of the broader decision-making process.

Flexibility and control

One of the standout benefits of Business Relief investments is the control retained by the investor. This sets Business Relief apart from other IHT strategies such as outright gifting, as the investments remain in the individual’s name and under their control. This means that if the investor’s circumstances change—such as the need for long-term care or unforeseen expenses arise—they can redeem the investment, subject to availability of liquidity. This makes Business Relief solutions particularly attractive for clients who want to plan tax-efficiently without fully relinquishing access to their funds.

Major reforms to Business Relief

The October 2024 Budget introduced significant reforms to Business Relief, due to take effect from April 2026. These changes will have meaningful implications for estate planning strategies and may lead investors to revisit existing plans.

Currently, assets that qualify for Business Relief are eligible for 100% relief from IHT. From April 2026, a new cap will apply, where the first £1 million of qualifying business and agricultural assets will continue to benefit from 100% relief, and any qualifying assets held above £1 million will receive only 50% relief, meaning the effective IHT rate will be 20% on the excess. This £1 million limit applies on a combined basis to Business and Agricultural Relief, and will remain fixed until 2030, after which it will increase in line with inflation.

Currently, qualifying shares listed on the AIM market receive full (100%) relief; however, from April 2026, the relief on AIM shares will reduce to 50%. According to HMRC data, the total IHT relief attributable to AIM shares in 2021/22 was approximately £185 million. The updated policy may, therefore, raise just £90 million of tax revenue per year, which leads us to question whether the disruption to investors is proportionate to the financial benefit for the Treasury.

Investors with significant AIM holdings must now consider whether the reduced tax efficiency justifies restructuring their investment portfolio. While recent AIM performance has been underwhelming, these shares may still offer long-term growth potential and merit inclusion depending on an individual’s risk profile and objectives.

The Importance of a holistic approach

Whilst this article has focused on Business Relief, and changes to the rules from next April, this solution is only one of a range of options that can be used to mitigate a potential IHT liability on death. By taking a holistic approach, tailored to your individual circumstances, our advisers can consider other options, such as gifting, the use of trusts and insurance products, as alternatives to Business Relief. Often when dealing with complex IHT planning needs, a combination of more than one of these options can provide the correct balance between tax efficiency, control, and risk.

Speak to one of our experienced advisers to discuss the implications of IHT on your potential estate and to discuss ways to reduce, or indeed avoid, a tax bill on your death.