The objective of many investment strategies is to focus on capital growth. Whilst this may well be appropriate for those accumulating pension savings or investing for the next generation, there is often an increased need for additional income to supplement pension income as we move into later life.

Retirees are not the only cohort where income production carries greater importance. Trustees of interest in possession trusts need to ensure that life tenants receive an attractive and consistent level of income. Higher levels of natural income can also allow greater gifts out of surplus income for Inheritance Tax (IHT) planning. Finally, individuals privately funding long term care could narrow the shortfall between pension income and care fees by selecting high yielding investments.

The CDI portfolio range includes four portfolios designed to provide investors with an attractive and consistent level of income. Whilst the portfolio income yield is a key consideration during the portfolio construction phase, the FAS Investment Committee also aim to ensure that capital growth is also targeted, as a hedge against inflation. Furthermore, as capital values increase over time, additional income can be generated from the higher capital value.

Our risk-rated options

Our advisers regularly review discretionary managed portfolios offered by alternative managers that are aimed at investors seeking income. All too often, these portfolios offer disappointing levels of natural income. The three core income options offered within the CDI portfolio range have been specifically designed to meet the needs of investors seeking a balance between capital appreciation and providing an attractive and sustainable income yield.

- CDI Defensive Income takes a low-to-medium risk approach, investing up to 35% of the portfolio in global equities. The balance of the portfolio is invested in global fixed interest securities, cash and alternative investments, to provide good levels of diversification. As a result, the portfolio has historically only displayed moderate levels of volatility. The current income yield offered by this portfolio is 4.02% per annum.

- CDI Balanced Income takes the middle ground between risk and reward, investing up to 65% in equities, and is suitable for investors comfortable with medium levels of risk and volatility. Given the increased allocation to equities, this portfolio offers a greater balance between capital appreciation and income production than CDI Defensive Income. Nonetheless, the portfolio offers an attractive yield, which is currently 3.44% per annum.

- CDI Progressive Income has a higher allocation to equities than CDI Balanced Income, allocating up to 85% in equities. This provides additional scope for capital appreciation, whilst maintaining an attractive income yield, and is suitable for those investors who are comfortable taking a medium-to-high level of investment risk. Despite the greater allocation to equities, the portfolio currently provides an attractive income yield of 3.27% per annum.

The consistent and disciplined approach adopted by the FAS Investment Committee considers the levels of volatility within every CDI portfolio at each quarterly review stage, to ensure that they remain consistent with the levels displayed by the benchmark. When undertaking the quarterly portfolio review of the CDI Income models, the Investment Committee take additional care to consider the impact of any changes on the investment portfolio income yield.

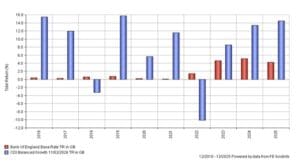

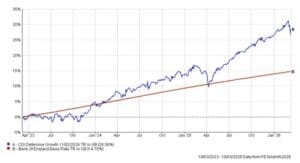

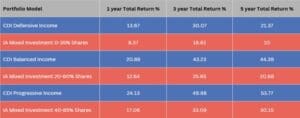

The three core Income portfolios continue to outperform the representative IA sector benchmarks over the short, medium and longer term. The table below demonstrates the total return (i.e. capital growth and income) achieved over the last 1, 3 and 5 years.

Performance data to 5th May 2026 Source: FE Analytics May 2026 – figures are net of fund charges, but do not include adviser or platform charges.

CDI High Income

Changes to the way pensions are treated for IHT purposes are leading many to reconsider their financial plans and making gifts out of surplus income is one method of reducing a potential IHT liability. As a result, we have seen growing demand for a discretionary managed portfolio that offers an even higher level of natural income.

The CDI High Income portfolio, which was introduced last year, holds around 40% in equities, with the balance held in fixed income, and contains an increased allocation to high yield bonds than in the core risk-rated mandates. The aim of the portfolio is to generate an income yield that comfortably exceeds the yield on the other three CDI income portfolios. To achieve this, the portfolio composition is naturally focused more closely on income production, although the portfolio also retains prospects for capital appreciation over the longer term. The current portfolio yield is 4.92% per annum.

Consistency of income

When investing to generate natural income, investors need to be mindful that the amount of income paid will differ from month to month. This is unavoidable, as investment funds offer different income payment schedules, with some paying monthly, others quarterly and a smaller number pay income twice a year. Furthermore, as the composition of the underlying portfolio within any fund will change over time, so will the level of income generated.

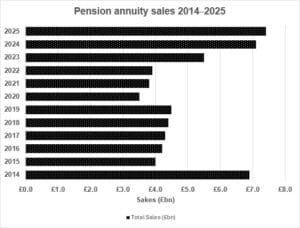

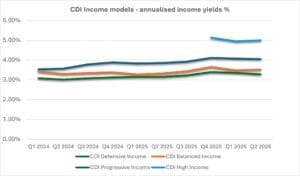

Despite these challenges, the FAS Investment Committee aim to keep the level of natural income paid by each of the four income portfolios consistent from quarter to quarter, so that investors can estimate their likely income with a degree of accuracy. The graph below shows the historic income yields generated by CDI Defensive Income, CDI Balanced Income and CDI Progressive Income since 2024, and the CDI High Income portfolio since it was introduced last autumn. As demonstrated, each of the portfolios has maintained a consistent level of natural income from quarter-to-quarter.

If you are disappointed by the level of natural income yield you receive from a portfolio designed to generate income, it may be a good time to review the investment approach adopted. Our independent advisers can undertake an impartial performance review of an existing portfolio and provide an unbiased assessment of performance against the CDI portfolio range.

Source: FE Analytics May 2026