After a brief hiatus, inflationary pressures are building once again. A combination of surging energy prices, persistent wage growth, and escalating geopolitical tension has seen inflation spike, and whilst levels of inflation are nowhere near the extreme levels seen in 2022 after the Russian invasion of Ukraine, it is sensible advice to pay careful attention to the impact of persistently higher inflation on investment performance.

Driven by global tension

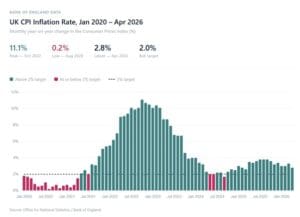

The Bank of England’s April 2026 Monetary Policy Report showed that annualised inflation rose to 3.3% and is expected to climb higher as the effects of elevated energy prices work their way through supply chains. This reality is in stark contrast to the predictions for low inflation and easier monetary policy that most economists were making at the start of the year.

Although a tentative ceasefire in the Gulf has been in place since April, oil prices remain elevated and even if a permanent resolution is found, it may take many months for oil supplies to return to levels seen before March. The supply shortage is also placing further pressure on global oil reserves, which is likely to keep inflation comfortably above the Bank of England’s CPI target of 2%.

We have all seen the impact of conflict in the Middle East when buying petrol or through household energy bills. The impact of these costs ripple through manufacturing, logistics and services, leaving businesses with a choice of either absorbing the higher costs, or passing these on. Food inflation is also set to rise far above the target rate, as farmers pass on the cost of fertiliser where prices have risen by almost 25% since February.

The hikes in the cost of essentials could lead to workers demanding higher wages to compensate and could lead to so-called “second-round effects” which further reinforces the upward pressure.

The hidden drain on investment returns

Many investors fail to keep the prevailing rate of inflation in mind when assessing the real performance achieved from an investment strategy. Whilst returns of 5% per annum may look attractive when taken at face value, if inflation runs at 4% per annum over the investment period, the real rate of return is effectively 1%.

Inflation has a variable impact on different asset classes. Where funds are held as cash, interest rates and inflation tend to move in the same direction, and over the longer term, simply holding cash savings may lead to a negative real return when the impact of inflation is taken into account.

Fixed income investments, such as government and corporate bonds, are also vulnerable to the eroding impact of inflation. Most bonds pay a fixed rate of interest, which may become less attractive in real terms in periods of higher inflation. As a result, bond prices can come under pressure. The same can be said for commercial property investments, where rental income is typically fixed for the duration of a lease.

As companies tend to raise their prices to protect their margins when inflation is elevated, equities can act as a hedge against rising inflation. Such conditions tend to favour companies with genuine pricing power. Likewise, infrastructure can prove more resilient as the cost of long-term maintenance contracts are often inflation linked.

The impact of inflation on the wider economic outlook also plays a key role in how different asset classes perform. If consumers react negatively to the effects of higher inflation and reduce spending, this can hurt the profits of those companies that rely on buoyant consumer confidence and dent the outlook for growth across the wider economy.

Protecting your portfolio

Investment markets are often able to withstand a modest bout of short-lived inflation; however, the longer inflationary pressures persist, the greater the impact. It is also worth remembering that investment markets are a predictive mechanism – investors are considering returns in the future, and if the outlook appears to worsen, investor sentiment may weaken.

There are, however, ways to protect your investments against inflation. In the case of cash savings, ensuring that savings are held in accounts paying attractive rates of interest can help offset at least some of the eroding impact of higher inflation. Accepting low interest rates in a period when inflation is higher, is likely to reduce the real spending power of savings.

Holding bonds with shorter durations can help avoid the worst impact of an extended bout of higher inflation, as they are less sensitive to upward movements in interest rates, which is often a policy response by central banks.

Whilst acting as a modest hedge against inflation, equity values can come under pressure from wider concerns over the health of the economy and outlook for interest rates. As shown during 2022, when the S&P500 index fell by over 18%, the level of insulation provided may be limited; however, companies in sectors with resilience and pricing power could outperform in such conditions.

Investment markets have enjoyed strong returns over recent months, building on the solid performance in 2025. Whilst inflationary fears persist, these are currently being somewhat overlooked, given the continued investor confidence in areas such as Artificial Intelligence; however, the longer energy prices remain elevated, the greater the likelihood that investor focus will shift to the wider economic impact.

Through our CDI discretionary managed portfolios, the FAS Investment Committee have taken a relatively cautious position across the range of models. The Committee have maintained an overweight position to short-dated bonds across fixed income allocations for the last 12 months and have positioned equity allocations to provide exposure to more value and defensive strategies to complement positions in high growth areas. Higher levels of cash are also being held across the range of CDI portfolios.

If you wish to discuss how your portfolio is positioned, then speak to one of the team to start a conversation.