For businesses that find themselves holding significant cash reserves, leaving funds idle in a business bank account, earning little or no interest, is rarely the most efficient strategy. Whether the surplus cash has arisen from profitable trading, the sale of an asset, or simply disciplined cash management, company directors should consider the benefits of keeping surplus funds productive, whilst balancing prospective returns, access to capital and risk.

Most companies will aim to keep a safe operating balance held on immediately available cash. The amount that a company should hold as cash varies depending on a range of factors, including fixed operating costs, anticipated expenditure, Corporation Tax and other liabilities, together with any expected variance in forthcoming trading conditions. We always recommend directors consult with their company’s accountant to help determine the most appropriate level to hold as immediate working capital.

Once immediate needs have been determined, it is important to look to keep additional funds productive, as not doing so presents a missed opportunity to generate additional returns on idle funds but also leaves company cash exposed to the eroding impact of inflation. It is sensible to identify the investment time horizon for any funds not held on immediate cash, to divide funds into a proportion that is easily accessible and separate funds that can be committed to longer-term investments.

Savings options

Business savings accounts provide a straightforward option. Easy access savings accounts tend to offer lower rates of interest, but provide quick access to funds, which may prove invaluable if the business needs to deploy funds at short notice. Beyond immediate access, banks and other financial institutions offer notice and fixed term deposit options, which offer higher rates of interest, but require cash to be locked away for a defined period. In the case of fixed term deposits, the bank will almost certainly not allow earlier access to funds during the fixed term, and therefore caution should be employed to make sure sufficient liquidity is maintained.

Corporate investments

Businesses are not restricted to holding surplus company funds as cash. Investing surplus company funds can generate improved returns to those available on deposit; however, care is needed to select the right mix of asset classes, considering when funds may conceivably be needed, and the level of risk that the directors feel comfortable with.

The first option to consider are money market funds, which are pooled investments that invest in fixed and floating rate notes, high-quality debt instruments and short-dated gilts and corporate bonds. Despite the composition of a money market fund, the fund is not risk free, although returns offered are generally higher than cash deposits.

Companies seeking to employ company cash more effectively could consider investment grade corporate and government bonds, with the aim of generating better returns than those offered by money market funds. When investing in fixed income securities, inflation risk can effectively be reduced by selecting bonds with short dates to redemption.

For company funds that can be invested for a longer period, a diversified portfolio of equities (shares) could provide greater returns, albeit with higher levels of investment risk. By constructing a portfolio across these asset classes, in combination with a sensible strategy for short term cash, businesses can look to build a portfolio designed to keep surplus funds productive, whilst meeting liquidity requirements.

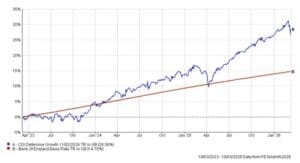

The graph below demonstrates the performance of the CDI Defensive Growth portfolio, a discretionary managed portfolio taking low-medium levels of investment risk, compared to a deposit account that tracks the Bank of England base rate, over the last 3 years. The graph shows the total return achieved, i.e. with income reinvested, but does not take into account investment management or platform charges.

As demonstrated by the graph, by taking a relatively modest level of investment risk, an invested portfolio has historically outperformed returns on cash, although some investment volatility will have been tolerated.

HMRC investment company rules

In our experience, directors are often unaware of HMRC rules when investing surplus funds held by a business, which can have significant consequences if not followed, including the potential loss of Business Asset Disposal Relief, which delivers a reduced Capital Gains Tax rate when directors sell shares in a “trading company”.

HMRC broadly define a “trading company” as one where the majority of the activities undertaken relate to a trade, rather than the investment activity itself. As a rule of thumb, if

20% or more of the company’s income is derived from investments, or 20% of the directors’ time is spent dealing with investments, or 20% of the company’s assets are held in investments, this could jeopardise a company’s trading status in the eyes of HMRC. These are, however, only guidelines, and we regularly liaise closely with company accountants to review the financial position of the company and the implications of any investments held.

Streamlined solutions

When speaking with company directors, we often find investment of surplus funds to be something of an afterthought; however, with sensible planning and expert advice, businesses can aim to keep surplus funds productive.

Thanks to our independent status, we have access to a range of investment platforms that can provide an ideal solution for surplus company cash. Through careful due diligence, we have identified UK based platforms that offer readily accessible savings and fixed term deposits via a range of renowned deposit takers, but also provide the ability for a discretionary managed or advisory investment portfolio to be held on the same platform. This provides a streamlined solution, easing the administrative burden and providing clear visibility.

We are very used to helping businesses invest surplus cash effectively. We can construct bespoke investment portfolios aimed to match the time horizon and risk profile for the funds in question, or manage funds on a discretionary managed basis, thus ensuring the portfolio is regularly reviewed and rebalanced.

If you are a director of a company that holds surplus funds, speak to one of our independent advisers about the options available to deploy those funds more productively.