Chancellor Rachel Reeves delivered the Government’s Spring Statement on 26th March. Whilst not a full-blown Budget, pressures on the UK economy from various angles meant that the Statement contained rather more than just an update to Budget forecasts. As expected, no changes to tax legislation were announced; however, there are several key takeaways which investors should consider.

Individual Savings Account (ISA) consultation

Buried in the depths of the Statement, the Government confirmed that they will undertake a review of the current ISA rules. The aim of the review will be to look to “boost the culture of retail investment” and will consider whether the balance between cash and investments is appropriate. This appears to be a clear indication that the Cash ISA is the main target of the consultation, rather than the Stocks and Shares ISA, and therefore the impact on investors could be limited. Savers, however, could see changes to the amount that can be saved within a Cash ISA, although there is no indication as yet as to how the Government could implement any changes to the existing ISA framework. We would expect further clarity as we head towards the Budget in the Autumn.

Increased tax receipts

Amongst the slew of data presented with the Statement, projected tax receipts highlighted the impact of recent changes to tax rules when assets are sold, and on inheritance. The Office for Budget Responsibility (OBR) expect Inheritance Tax (IHT) receipts to have climbed to £8.4bn for the 2024/25 tax year, an increase of 11.6% on the receipts from the previous year. Even more stark is the projection that IHT receipts will reach £14.3bn by 2029/30, a 70% increase over the next five years. The expected increase is due to the inclusion of pensions within the scope of IHT from April 2027, the changes to Agricultural and Business Reliefs, and the ongoing impact of the frozen Nil Rate Band.

Capital Gains Tax (CGT) is also forecast to bring increased funds into the Treasury over the rest of this parliament. The CGT exempt amount (i.e. the net amount of gain that can be made before CGT becomes payable) has been slashed from £12,300 per year to just £3,000 per year in successive Budgets, and the rates of CGT payable by investors increased immediately after the Budget last October. The OBR have forecast that CGT receipts will rise sharply to £19.7bn for the 2025/26 tax year, an increase of 48% on the amount received in the current Tax Year and reach £25.5bn by the end of this parliament in 2029/30.

With more estates being liable to IHT, and investors increasingly unable to avoid CGT, the forecasted figures are a timely reminder of the need to ensure that your financial plans are as tax efficient as possible.

Growth downgraded

The UK economy has effectively stalled over recent months, with GDP data showing very marginal gains. It was, therefore, no surprise that the OBR have downgraded their growth forecast for the UK economy in 2025 from 2% to 1%. Other leading forecasts show a weaker projection, with the Bank of England reducing their growth forecast from 1.5% to 0.75% in February.

Both forecasts may, however, be too optimistic. Households have just been hit with a succession of price hikes, from Council Tax increases to a jump in utility bills. This is likely to continue to supress consumer confidence as households grapple with higher essential expenditure. Businesses have just been impacted by the increase in minimum wage, and hike in employer’s National Insurance. This could lead to rising unemployment, and higher prices, as businesses look to offset the higher costs.

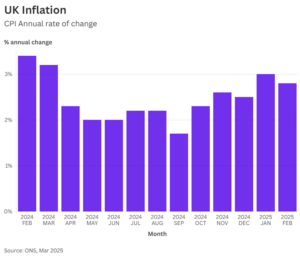

Inflationary pressure

The Chancellor received a welcome piece of news before the Statement was delivered, when the annual rate of inflation, measured by the Consumer Prices Index, fell from 3% to 2.8% in February. This does, however, remain above the Bank of England target rate of 2%.

Most economic forecasters expect inflation to rise again over the rest of this year, as a combination of tax hikes on business and higher energy costs force prices higher. In their latest inflation report, the Bank of England predict that inflation will hit 3.7% by the middle of the year, before falling back gradually.

Amidst an increasingly uncertain outlook for the global economy, we question whether these projections have properly considered the potentially disruptive impact of tariffs imposed by the US administration. On the same day as the Spring Statement, the US announced new tariffs on the import of cars and car parts from overseas, which could directly affect UK exports of luxury vehicles to the US, which is a major buyer of British marques.

Considering the range of factors, the balance of risks may point to inflation moving higher than is currently projected. This could, potentially, limit the scope for further interest rate cuts as 2025 progresses.

What should investors do?

Whilst the Spring Statement did not introduce any changes to tax legislation, it reinforced the weak outlook for the UK economy and underlined the need for investors to consider the tax-efficiency of their financial arrangements.

The ISA allowance remains a valuable tax break and a cornerstone of many financial plans. Naturally, we wait with interest to learn further details on the government review of ISA regulations; however, the indication is that Cash ISAs are more likely to be impacted than Stocks and Shares ISAs.

The projected increased tax receipts from IHT and CGT are a timely reminder of the need to plan ahead to minimise your exposure to either of these taxes. Undertaking estate planning can help reduce the potential IHT liability on your death and leave more of your estate to your loved ones. Similarly, structuring investments with tax-efficiency in mind can help reduce the likelihood of a CGT liability when assets are sold.

Our experienced advisers can carry out an impartial and holistic review of your financial arrangements and suggest changes that promote tax-efficiency and are tailored to your financial goals. Speak to one of the team to start a conversation.