The success of any investment strategy is determined by the performance of the investments selected, and the length of time that the investments are held. Maths also plays an important part in contributing towards the returns achieved, as growth, which is accumulated or reinvested, benefits from a compounding effect, which helps accelerate investment returns over time.

In simple terms, compound returns are earned on both the capital investment and investment growth already achieved. This additional “growth on growth” has a cumulative effect and helps investments grow exponentially. Whilst incredibly powerful, the impact of compound investment returns reinforces the need to ensure that your investment funds perform well. If funds underperform over a sustained period, this can lead to substantially lower returns, when considering investment strategies that are in place for many years, such as a pension.

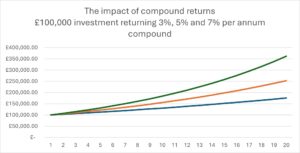

To demonstrate the impact of compound returns, take the example of Alice, whose pension plan is valued at £100,000. She plans to retire in 20 years’ time and does not expect to contribute further to this plan. If the investment achieves a rate of return of 3% per annum compound, the value at the end of the 20-year investment period would be £175,000. Increasing the investment return to 5% per annum compound would see the value at the end of the 20-year investment period increase to £252,000. Achieving an even higher return of 7% per annum compound would see the value at the end of the 20-year investment period rise significantly higher to £361,000.

As demonstrated on the graph, the rate of growth accelerates due to the impact of compound returns. By achieving compound returns of 7% per annum, rather than 3% per annum, at the end of the 20-year investment period, the value of Alice’s plan would stand at more than double the value that would have been achieved if returns were only 3% per annum.

This simple example demonstrates the power of compound returns; however, other real-world factors need to be considered. It is important to reflect on the eroding impact of inflation on investment returns, particularly over a longer timeframe, such as a working lifetime. The spending power of money falls over time, and this factor needs to be considered when undertaking calculations on future investment returns. The annual return achieved from risk assets, such as equities, bonds, and property, will also fluctuate from year to year, and examples using a fixed linear rate of return are unlikely to prove accurate. Finally, the impact of tax and charges on investment returns also need to be factored in.

Why performance needs to be reviewed

Given the cumulative effect of underperformance, it is important to keep any portfolio strategy and investment fund selection under close review. We often meet with new clients who have held the same investments within a pension, investment bond or Individual Savings Account (ISA) for an extended period, and in many cases, the performance of the portfolio held has lagged the performance of other funds investing in a similar portfolio of assets, with broadly the same level of investment risk.

This is particularly true when we undertake analysis of legacy investment products, which were purchased some time ago. The financial services industry is constantly evolving, and many historic investment products offer a limited range of investment options, which can hinder growth over the longer term. We often see other drawbacks with legacy products, such as high charges and exit penalties.

Taking an independent view of the universe of investment funds is, in our opinion, a vital component that helps drive investment returns. Products offered by restricted advisers tend to offer investors a limited menu of fund options from which to select, with many of the choices often limited to in-house investment funds. Whilst some of these funds may perform well compared to sector peers, it is often the case that we see sustained underperformance, the effect of which becomes more apparent over time due to the compounding effect. Even small marginal gains in performance can compound into a significant difference in outcome. For example, on an investment of £100,000 held over 40 years, a slight increase in return achieved, from 4% per annum to 4.5% per annum, would result in additional growth of over £94,000 being achieved (before the effect of charges and tax).

Compound returns are a powerful factor that is hard to ignore; however, investors need to give sufficient time for the compounding effect to impact investment returns, as the effect becomes more powerful, the longer an investment is in place. This is particularly true when long term regular savings, such as pension contributions made over many years, benefit from the power of compounding.

How to take advantage of compound returns

Compounding is a powerful driver of investment returns, and investors should be aware of the need to review their investment portfolio regularly, so that changes to underperforming assets can be made. As the examples have shown, even a small difference in performance over time can have a major impact. It would also be wise to consider investment product selection, as legacy investments can hinder growth over time due to limited fund choice and higher charges.

Speak to one of our experienced advisers to review your existing investment or pension plans. We can analyse investment performance and where appropriate recommend changes that aim to take full advantage of the power of compound returns.