The Budget announced a five-year freeze to the standard lifetime allowance.

The standard lifetime allowance (SLA) is an important pensions number. It effectively sets the maximum tax-efficient value of all your retirement benefits, in the absence of any legislative protections (of which there are many). To the extent that the SLA is exceeded there is a special flat-rate tax charge which is 25% if the excess is drawn as taxable income and 55% if it is received as a lump sum.

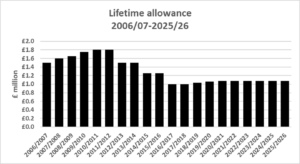

When the SLA was first introduced in 2006, it was set at £1.5 million, a level which equated to an annual pension income of £75,000, based on a standard legislative assumption of an annuity rate of 5%. The initial legislation set out increases for the SLA to £1.8 million in 2010/11. That proved to be the SLA’s highwater mark. It was frozen in the following year and then the first of three cuts were introduced. By 2016/17 the SLA was down to £1 million.

For three tax years from 2018/19 the SLA has been index-linked, but from April 2021 it will be frozen for half a decade at £1,073,100. Had the original £1,500,000 level been index-linked, the SLA would now be £2,082,100 – not far short of double the actual level.

The devaluation of the SLA has three consequences:

- The pension protected from the SLA tax charge has fallen. On the legislative basis which applies to defined benefit (final salary) schemes, it will now be £53,945. For defined contribution pension arrangements, such as personal pensions, the erosion is greater. Low annuity rates mean that £1,073,100 will buy an inflation-proofed income of just over £31,000 a year (before tax) for a 65-year-old.

- More people are being caught by the special tax charge. HMRC’s latest (sic) figures show over 4,500 SLA charge payers in 2017/18 against 1,240 five years earlier.

- The legislative protections, some of which date back to 2006, are all the more valuable.

If you think you might be affected by the SLA tax charge, either based on current benefits or when you reach retirement, take advice as soon as possible. You could find that from now on it is best to exclude pension contributions from your retirement planning.

If you are interested in discussing the above with one of our experienced financial planners at FAS, please get in touch here.

The value of your investment and income from it can go down as well as up and you may not get back the full amount you invested. Past performance is not a reliable indicator of future performance. The value of tax reliefs depends on your individual circumstances. Tax laws can change. The Financial Conduct Authority does not regulate tax advice.