New HMRC data show the popularity of this traditional perk could be waning.

Source: HMRC September 2020

There was a time when the company car was the fringe benefit that every employee wanted. You had ‘made it’ once you had the keys to a car with no worries about servicing, insuring or, sometimes, even fuel costs. It could also make plenty of tax sense, as the cost of the car was not fully reflected in the amount on which tax was charged. Go back far enough and two company cars were not uncommon for some senior executives.

Unsurprisingly, the days of company cars as tax-efficient remuneration have largely passed, other than for electric vehicles. The government approach to company cars brings to mind the comment of Jean-Batiste Colbert, a 17th century French Minister of Finance, who said “the art of taxation consists in so plucking the goose as to procure the largest quantity of feathers with the least possible amount of hissing”.

Some 400 years later, successive UK chancellors have steadily notched up the company car benefit scales to raise additional revenue from a stable to shrinking number of company car drivers. For example, the latest HMRC data show that between 2010/11 and 2018/19, the average company car taxable value has risen by 57% against a 19% increase in inflation over the same period.

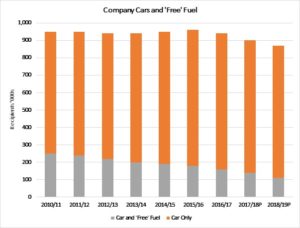

Similarly, the taxable value of ‘free’ fuel (i.e. employer-funded fuel) has risen by 44%. As the graph shows, the popularity of ‘free’ fuel has steadily fallen – only about one in eight company car drivers now pays nothing to fill up their tank. If you are one of that minority, do make sure you have enough private mileage to justify the tax you pay. The main reason for the drop in ‘free’ fuel numbers is that for many employees, the tax bill would be greater than their personal refuelling cost.

The gradual demise of the company car is a lesson in how the tax system can subtly alter over time. A major revamp in the treatment of salary sacrifice schemes introduced in 2017 changed the tax landscape for other fringe benefits, too. The one that has survived and remains attractive – at least for now – is salary sacrifice to fund pension contributions.

If you are interested in discussing the above with one of our experienced financial planners at FAS, please get in touch here.

The value of tax reliefs depends on your individual circumstances. Tax laws can change. The Financial Conduct Authority does not regulate tax advice. The value of your investment and income from it can go down as well as up and you may not get back the full amount you invested. Past performance is not a reliable indicator of future performance.