New statistics from HMRC show over £300bn invested in cash ISAs.

Source: HMRC.

One of the many knock-on effects of the pandemic has been that HMRC’s annual updating of statistics has suffered delays. As a result, details of ISA subscriptions and holdings for 2019/20 have only just emerged. Among many interesting facts, the data shows:

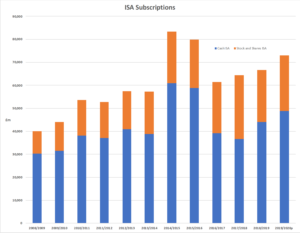

- Despite ultra-low interest rates, the amount of money invested in cash ISAs has continued to grow. In 2019/20, £48.75 billion of subscriptions were received, more than twice as much as was invested in stocks and shares ISAs.

- The increase in the maximum overall ISA contribution to £20,000 in 2017/18 (from £15,240) has still not driven total annual subscriptions above their 2014/15 peak.

- Lifetime ISAs (LISAs), launched in 2017/18 to no great fanfare, have since grown in popularity, with 2019/20 subscriptions more than double those of the previous year. This jump may have been helped by the closure to new investors of the Help to Buy ISA in December 2019.

- For the first time, over one million subscriptions were made to Junior ISAs (JISAs) in 2019/20, with total investment of £974 million.

- The total amount invested in ISAs (excluding JISAs) in April 2020 was just under £620 billion, of which just over half was held in cash ISAs. The cash proportion would likely be substantially smaller today, as the value of stocks and shares ISAs were depressed in April 2020 when the first lockdowns got underway.

The continued dominance of cash ISAs is, at least in part, a reflection of the lack of financial planning advice received by many ISA investors. The personal savings allowance, introduced in 2016/17, means that basic rate taxpayers (calculated using UK-wide rates) pay no tax on their first £1,000 of interest and, similarly, £500 of interest is tax free for higher rate taxpayers.

At current interest rates, it takes a considerable amount of capital to exceed even the lower threshold so taking out a cash ISA could be of questionable value compared with an ordinary deposit, which might pay a higher interest rate. However, the ISA framework could be useful to you in other ways, so advice is essential before taking any action on a cash ISA.

If you are interested in discussing the above with one of our experienced financial planners at FAS, please get in touch here.

The value of your investment and the income from it can go down as well as up and you may not get back the full amount you invested. Past performance is not a reliable indicator of future performance. Investing in shares should be regarded as a long-term investment and should fit in with your overall attitude to risk and financial circumstances. The value of tax reliefs depends on your individual circumstances. Tax laws can change. The Financial Conduct Authority does not regulate tax advice.